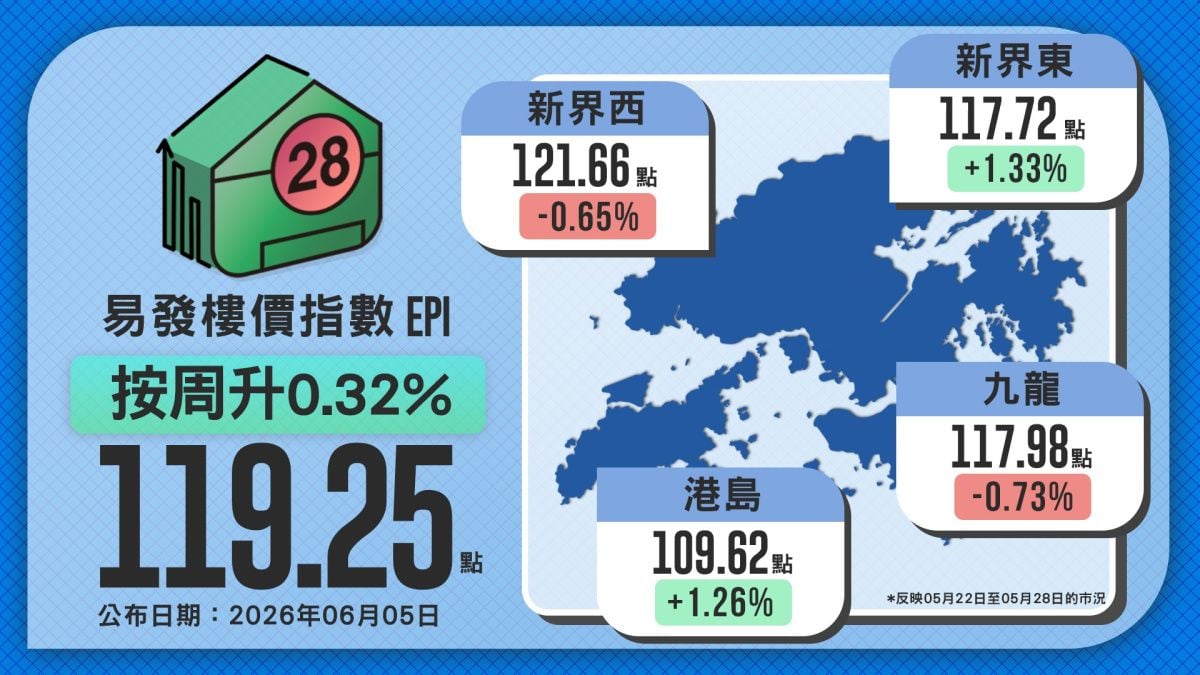

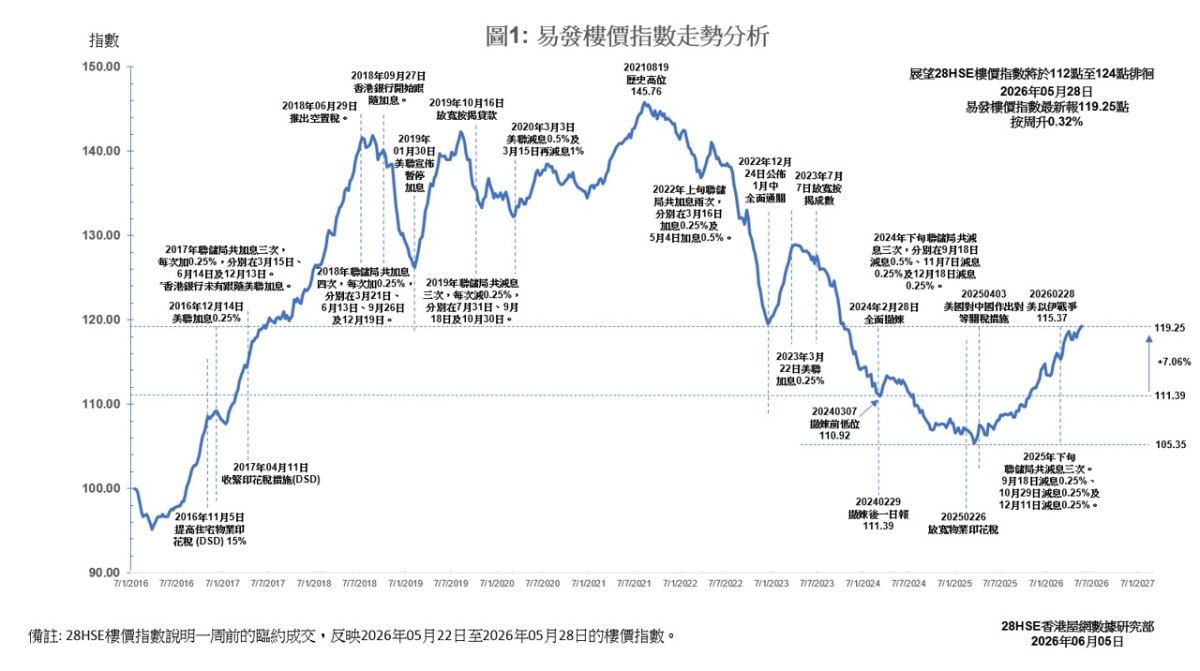

The Eva Property Index (EPI) for the last week of May stood at 119.25 points, representing a week-on-week (WoW) increase of 0.32% and marking a three-week consecutive rise. Year-to-date, property prices have accumulated an increase of approximately 5.1%, though they remain about 18.19% below the historical peak of 145.76 points recorded in August 2021.

Currently, primary market sales continue to dictate the trajectory of secondary property prices. This week, the four major regional property price indices exhibited mixed performances, with two rising and two falling. Capital flows were primarily influenced by the pace of new project launches. In New Territories East (NTE) and Hong Kong Island, the temporary absence of large-scale new project launches redirected purchasing power back to the secondary market, bolstering owners' asking prices and driving up regional property values. Conversely, robust primary sales in Kowloon and New Territories West (NTW) absorbed a substantial number of buyers. Compounded by a mismatch in luxury property listings, secondary owners were compelled to reduce asking prices to secure sales, placing temporary downward pressure on property prices in these districts.

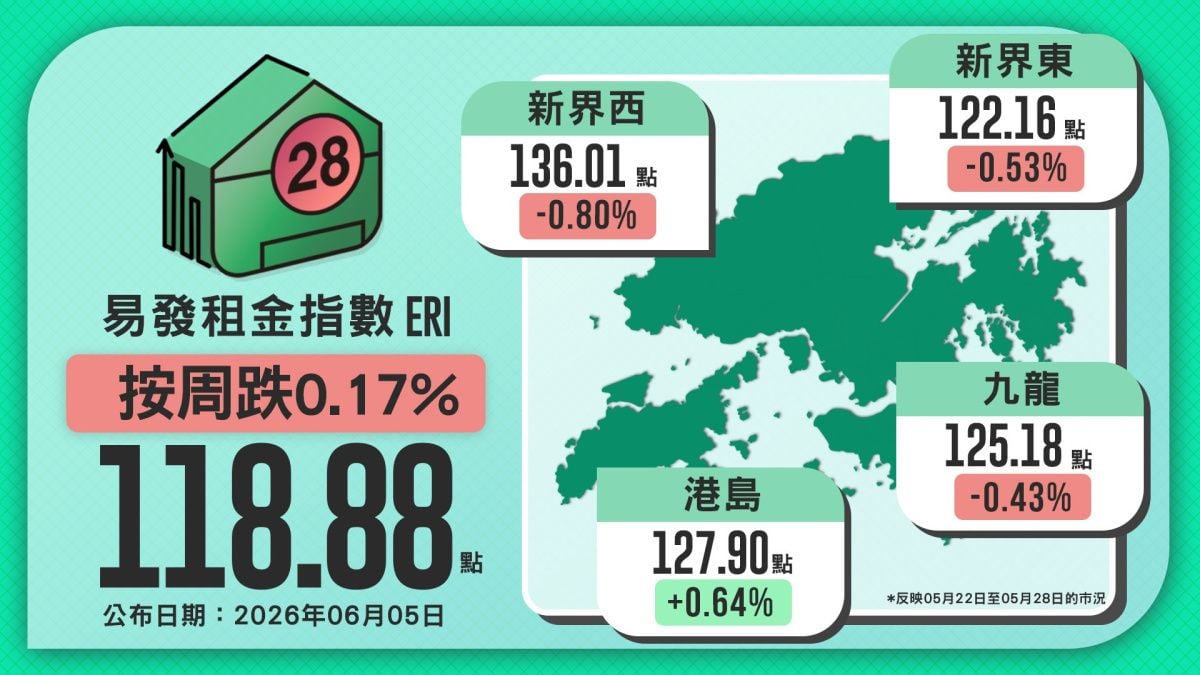

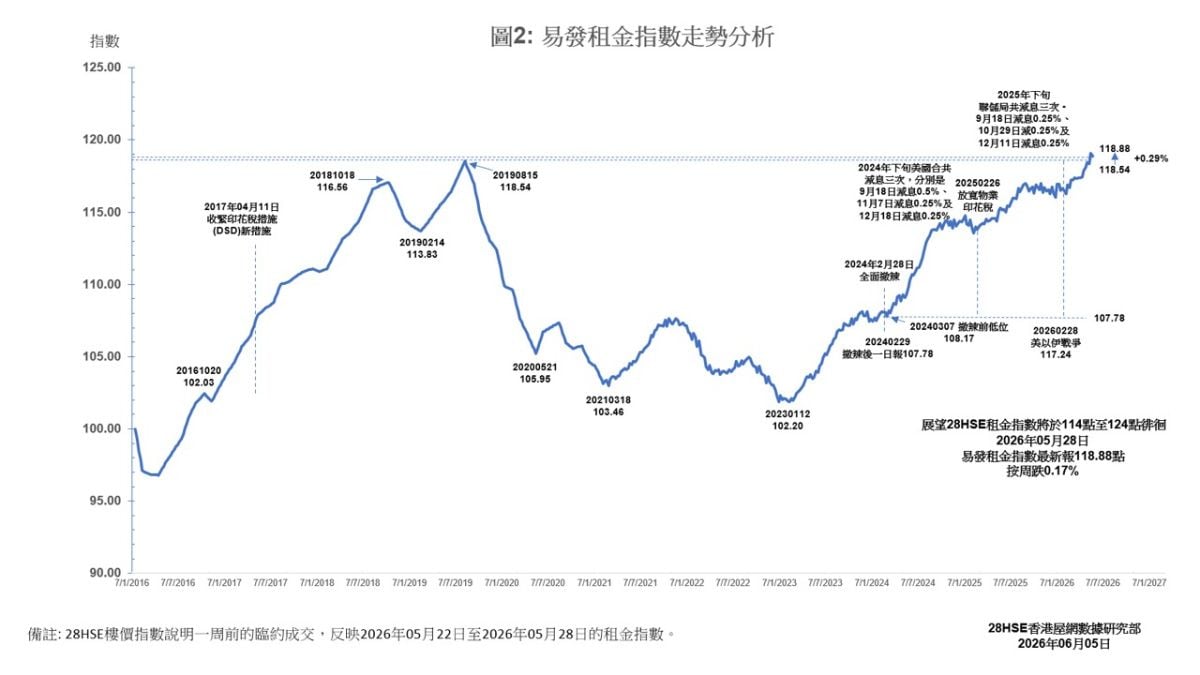

In the rental market, the Eva Rental Index (ERI) experienced a slight WoW decline of 0.17% this week, settling at 118.88 points. However, it has sustained a level above 118 points for five consecutive weeks and remains 0.29% higher than the previous peak of 118.54 points recorded in August 2019. With the summer holidays approaching, rental demand from non-local students is expected to materialize gradually. While short-term fluctuations in rents are anticipated, the overarching trend remains upward. The market is likely to witness continuous high-priced leasing transactions, propelling the rental index to steadily challenge new highs.

Looking ahead, developers' project launch strategies and pacing, coupled with the US Federal Reserve's interest rate trajectory, will continue to steer the direction of property prices. Notably, the "buy-is-cheaper-than-rent" phenomenon (where monthly mortgage payments are lower than rent) has emerged in numerous housing estates. To avoid missing the optimal window to enter the market, some tenants may transition from renting to buying, a trend anticipated to attract long-term investment capital. On the rental front, benefiting from incoming professionals and students securing leases in advance with upfront payments, along with the impending summer leasing peak, rigid housing demand will increase significantly. Consequently, both overall property prices and rents are projected to maintain a steady upward momentum.

Regional Prices Mixed: NTE and Hong Kong Island Surge Over 1%

Regional property price indices displayed a mixed performance this week. NTE recorded the most significant gain, halting a two-week decline to close at 117.72 points, up 1.33% WoW. Hong Kong Island also demonstrated a positive trend, rising 1.26% WoW to 109.62 points. On the other hand, Kowloon experienced a second consecutive week of decline, dropping 0.73% WoW to 117.98 points, while NTW ended its recent upward streak, falling 0.65% WoW to 121.66 points. Overall, regional price fluctuations were primarily driven by local new project sales and the quality of secondary listings.

The notable price increase in NTE this week was largely attributed to the current lack of major focal new projects in the district. The slowdown in the sales of primary market inventory prompted purchasing power to flow back into the secondary market. Driven by buyer demand, secondary owners generally narrowed their negotiation margins, pushing prices upward. During this period, primary transactions were mainly concentrated in La Mirabelle I and Cloudview, recording 12 and 10 transactions respectively. This reflects that in the absence of a primary market focal point, capital is gradually shifting to the secondary market in search of available properties.

Property viewing data further corroborates this trend. According to Midland Realty, the top four indicator estates in NTE recorded approximately 167 viewing appointments during the three-day Buddha's Birthday long weekend (May 23 to May 25), representing a surge of about 40.34% compared to the 119 groups recorded in the preceding weekend (May 16 to May 17). Data from Hong Kong Property Services also indicated that two major indicator estates in the district recorded around 183 viewing groups during the same period, a WoW increase of 12.27%. These figures suggest that prospective buyers are capitalizing on the opportunity to absorb reasonably priced units in the district's secondary market.

Regarding the outlook for NTE, developers' strategic moves reveal confidence in the market's prospects. It is reported that Henderson Land will repossess Parkwood in Tai Po and terminate its student hostel lease agreement with the Chinese University of Hong Kong upon lease expiration in August this year. Market analysts point out that as property transactions rebound and prices gradually stabilize entering 2026, the developer plans to relaunch the project in the second half of the year to boost revenue. This move underscores developers' optimism regarding the underlying support for the district's property market.

On Hong Kong Island, the price trajectory mirrored that of NTE, registering a WoW increase of 1.26% this week. Primary market transactions in the district remained relatively stable, primarily supported by 12 transactions at the Headland Residences. Given the lukewarm primary sales, secondary owners observed slightly weakened buyer absorption capacity but adopted a firmer stance on asking prices to avoid selling at a discount. This reluctance to sell has become the primary driving force supporting the upward movement of Hong Kong Island's property prices.

Property viewing activities on Hong Kong Island were equally robust. Midland Realty data showed that two major indicator estates in the district recorded approximately 41 viewing appointments during the Buddha's Birthday long weekend, up 24.24% WoW. Hong Kong Property Services' statistics also highlighted that two major indicator estates recorded around 188 viewing groups during the same period, a WoW increase of 39.26%. The sharp rise in foot traffic during the festive long weekend provided corresponding support for secondary property prices in the district.

In contrast to NTE and Hong Kong Island, the Kowloon property price index fell for the second consecutive week. The strong sales performance of primary inventory in the district continued to absorb market purchasing power, exerting pressure on the secondary market and forcing owners to widen their negotiation margins to enhance property competitiveness. During this period, projects such as the MIAMI QUAY series, Phase 2 of Highwood, Phase 3 of One Victoria Cove, and Victoria Voyage series recorded between 8 and 25 primary transactions each. The robust sales of new projects diluted the pool of secondary buyers, leading to temporary downward pressure on overall regional prices.

May Chu, Managing Director of Love Property Agency Limited, analyzed that another primary reason for the decline in Kowloon's property prices lies in the sluggish secondary transactions in traditional luxury residential areas such as Ho Man Tin and Kowloon Tong. Currently, the district suffers from a chronic shortage of premium vacant listings. Some listings in estates like Parc Palais and Parc Oasis are either sold with existing tenancies or possess flaws, making them unavailable for viewing, while estates like Mantin Heights only have mid-to-low floor units remaining. As buyers in this district are predominantly stringent owner-occupiers, the mismatch in listings has stalled high-priced transactions. The sporadic transactions recorded this week were mostly low-priced or secondary-tier units, which directly dragged down the district's property price index.

Despite the pressure on the secondary market, primary market sentiment in Kowloon remains fervent. After a five-year hiatus, THE HENLEY I released an additional 48 units at a discounted average price of $31,894 per square foot, representing an increase of approximately 11.25% compared to its previous price list in 2021. Concurrently, the new Kowloon Tong project Pavilia Rosa has uploaded its sales brochure and is preparing for tender. Developers' continuous project launches and price hikes have successfully invigorated overall market sentiment, which is expected to help regional property prices bottom out and rebound.

Regarding Kowloon's market outlook, Chu believes the fundamentals remain robust. Taking Pavilia Rosa as an example, 40 of the project's 109 units were sold via tender within a short period, reflecting an enthusiastic market response. Given the lack of large-scale new project supply in Kowloon Tong for the next 8 to 10 years, coupled with the unique advantage of its elite school network, the area will continue to attract affluent families from Hong Kong and the Mainland. Overall, the temporary pullback in Kowloon's property prices is merely transitional. Supported by the dual factors of rigid demand and rare supply in core areas, it possesses excellent long-term downside resilience and upside potential.

Property prices in NTW also softened this week, primarily affected by the brisk sales of primary inventory in the district. The benchmark new project Lime Spark conducted its third round of sales this week, selling out all 87 units offered. Combined with 6 units sold via tender, a total of 93 transactions were facilitated, marking a stellar performance. The sales day attracted numerous bulk purchasers, with one buyer spending over $40 million to acquire six two-bedroom units. The strong sales of new projects absorbed a massive amount of purchasing power in the district, prompting secondary owners to increase their negotiation room and causing NTW property prices to soften accordingly.

Capitalizing on this momentum, the developer released an additional 51 one-to-two-bedroom units at Lime Spark the day following the sales. The new batch of units has a discounted average price of $19,149 per square foot, approximately 2.88% higher than the previous price list. Furthermore, the developer revised previous price lists, raising the prices of remaining inventory by up to 4.3%. For instance, a high-floor unit with a saleable area of 273 square feet saw its listed price increased from $5.872 million to $6.122 million. The developer's successive additional releases and price hikes reflect full confidence in the project's subsequent sales performance and the district's property market outlook.

In summary, this week's property price trajectory was characterized by "the primary market dominating the secondary market." In NTE and Hong Kong Island, which lacked new project focal points, the return of purchasing power drove up secondary transaction prices. Conversely, in Kowloon and NTW, robust new project sales absorbed buyers, which, combined with a mismatch in some luxury listings, exerted temporary pressure on secondary property prices.

Alex Cheung, Data Researcher at 28Hse Limited, analyzed that developers' launch pacing and pricing strategies remain the critical factors influencing the broader market. Furthermore, the US Federal Reserve's interest rate decisions will impact Hong Kong's bank mortgage rates and the subsequent property market outlook. With the "buy-is-cheaper-than-rent" phenomenon gradually becoming the norm in many estates, it is expected to attract numerous long-term investors and buyers with rigid demand. The overall EPI is projected to continue its steady upward climb in the short term, fluctuating between 112 and 124 points.

Rental Index Softens by 0.17%, Still 0.29% Above 2019 Peak

Following its record high last week, the ERI stood at 118.88 points, marking a marginal WoW decline of 0.17% but remaining above the 118-point mark for five consecutive weeks. Summarizing the trend for the year, the index has accumulated a 1.65% increase year-to-date and remains 0.29% higher than the historical peak of 118.54 points recorded in 2019. Overall, while Hong Kong's rental levels may experience short-term softening, the macro trend remains elevated.

Regarding regional index performances, the districts exhibited three declines and one increase. The NTW index reported 136.01 points (down 0.8% WoW); the NTE index stood at 122.16 points (down 0.53% WoW); and the Kowloon index reported 125.18 points (down 0.43% WoW). All three districts ended their recent consecutive upward streaks.

This was primarily due to below-market rental transactions recorded in certain estates. For example, a three-bedroom unit with a saleable area of 646 square feet at Marina Garden in Tuen Mun was leased for $15,500 per month. The effective rent of approximately $24 per square foot is lower than the 28Hse 90-day average of $26 per square foot. Similar situations were observed at The Arles in Fo Tan and Banyan Garden in Cheung Sha Wan, where the latest two-bedroom transaction rents per square foot were $48.2 and $43.5 respectively, both trailing their 28Hse 90-day averages of $51 and $45 per square foot. Such transactions, with rents slightly below the market average, led to a softening in the rental trends of the New Territories and Kowloon districts.

Chu analyzed that the decline in Kowloon's rents this week was mainly affected by the wave of new project handovers in the Kai Tak area, resulting in a short-term oversupply of rental listings. Landlords have consequently widened their negotiation margins. For instance, a two-bedroom unit at The Pavilia Forest II was leased for $19,000 after being on the market for over two months, a 24% reduction from the original asking rent of $25,000. Such rent reduction cases impact the district's overall rental trajectory and are expected to create a ripple effect across approximately 10 other new projects in Kai Tak, keeping rental prices in the district under pressure in the short term.

Contrary to the New Territories and Kowloon, the rental trend on Hong Kong Island defied the broader market, rising 0.64% WoW to 127.9 points and marking a two-week consecutive increase. The upward momentum in the district's rents was primarily fueled by leasing demand from Mainland students, which facilitated the leasing of certain units at more favorable prices. For example, a 253-square-foot one-bedroom unit at One ArtLane in Sai Ying Pun was leased by a Mainland student for $20,000 per month, translating to an effective rent of $79 per square foot, surpassing the 28Hse 90-day average of $74 per square foot. Additionally, a 245-square-foot one-bedroom unit at FINNIE in Quarry Bay was leased for $18,500 per month, with the rent per square foot reaching a high of $75.5, also exceeding the 28Hse 90-day average level of $66. Active high-priced leasing transactions have become the main driving force supporting the continuous climb of the Hong Kong Island rental index.

Looking ahead at the rental market trajectory, Cheung maintains his previous forecast, estimating that the ERI will hover at high levels between 114 and 124 points in the short term. As the traditional summer leasing peak approaches, the substantial demand for housing will increase significantly, driving up leasing transaction volumes and potentially leading some estates to set new record highs for per-square-foot rents.

Given that the index has already breached its 2019 historical peak, rents are expected to continue seeking new highs after digesting short-term volatility. In the long run, the overall rental trajectory for this year is projected to maintain a steady upward trend, with full-year growth estimated between 2% and 4%. In conclusion, the actual demand for housing in the market remains robust, which is believed to be sufficient to provide solid support for overall rents, keeping them firmly at high levels.

The above indices reflect market conditions from May 22, 2026, to May 28, 2026.