[28Hse 三地產焦點 第二十八期 2015年9月16日] 有保險公司推出廣告,以年僅7歲「美心妹妹」楊鎧凝任代言人,旁邊寫上「我想儲錢買樓」及「敢想,未來才會更精彩」字句。除地鐵站外,大家亦可於巴士車身見到有關廣告。

廣告一出街,即引起全城議論紛紛,有人認為7歲已講買樓是言之過早;有人則認為香港社會畸形,7歲諗買樓亦無可厚非;有人又覺得現時市民價值觀已被扭曲;有人又認為未雨綢繆並不是一件壞事。而筆者則認為這廣告概念有點誇張,但某程度反映現實。

現實生活中,父母幫兒女買樓、上車的情況並不罕見,新近有一例子更令人驚訝,迎海.駿岸(附圖為6座示範單位)買家陳先生表示,會以超過$700萬買入7座17樓單位,打算購入給予年僅3歲的小兒子,供他將來長大後作結婚用。他坦言,雖然覺得樓市會跌,但他表示不知道廿年後世界會怎樣,所以要睇長遠些,給兒子買定先。

的確,現在真的難以估計日後的世界會怎樣,樓價依舊會熾熱,還是已成功降溫?現在買定先,是賺還是蝕?我們真的無法預測。這概念其實某程度是大人以自己的價值觀套於小朋友身上,買樓理應是大人的事,而小朋友是天真的,但提早儲蓄買樓又是否真的不該?

根據2010年的報道,香港人首次置業的平均年齡約為31歲。而參考房委會對二手居屋買賣的統計調查(詳見附表2),顯示2011年4月至2013年3月期間買家的年齡層的分布,分為已補地價成交的公開市場和無需補地價的第二市場成交,當中公開市場的首次置業買家年齡中位數為34歲。

如果你不能「成功需父幹」,坦白說,現時作為香港人究竟幾時可以成功置業?筆者完全找不到有關資料,亦都不知道現時有多少業主是由父母出資協助。但現時香港的樓價熾熱,甚至可以用「顛」價來形容,真的可以像幾年前那樣努力工作,30餘歲就可以首次置業?根據早前《全球樓價負擔能力調查》,香港住宅樓價是全球最難負擔城市,樓價入息比率更由14.9倍,升至17倍,即市民連續17年不吃不喝才能置業。

認真想想,筆者認為單靠自己工作是不可能的,若以大學生一般是在21至22歲畢業,大約工作10年後就可買樓,儲首期的時間略嫌不夠。假設你購買一個$400萬的上車盤,6成按揭,首期是$160萬,若每月可儲$4,000,不作任何投資,10年可儲$48萬,和首期相差得太多。當然有人會說,人工會增加,儲得錢應會增加,但不要忘記樓價亦是會調整的,跌當然是好事,但如果升了,買樓一事變得更遙遠。

是次廣告用7歲小朋友任代言人,令筆者不禁想起香港長官梁振英於發表施政報告時,提及一名5歲小朋友詢問他「我長大後住哪裏?香港還有沒有足夠土地?」,外界有不少人質疑他說謊,認為小朋友不懂得提出此問題,認為他借小孩「過橋」。

究竟這些小朋友是被人借「過橋」,還是真的被社會逼成熟?筆者無從稽考,只是覺得孩子自小養成儲蓄習慣無壞,如果將每年的利是錢、零用錢存備,存下的金錢應不少,可用作買樓或其他用途的部分資金,這可算是另類的「成功需父幹」。

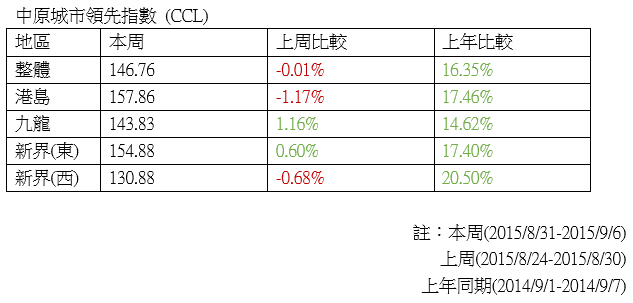

中原城市領先指數(CCL)最新報146.76(反映2015/8/31至2015/9/6 (預計簽署正式買賣合約時段) 的二手私人住宅樓價。一般在簽署臨時買賣合約後14日內簽署正式買賣合約。)按周微跌0.01%,而較上年同期上升16.35%。

本周九龍及新界(東)區均錄得升幅,分別新報143.83及154.88,按周上升1.16%及0.6%,而較上年同期分別上升14.62%及17.4%。而港島區則跌幅最多,按周下跌1.17%,較上年同期上升17.46%。而新界(西)區新報130.88,按周下跌0.68%,較上年同期上升20.5%。

-- 黃大仙盈利大廈 $418萬易手 --

世紀21富山地產樂富分行高級經理黃澤龍表示,日前錄得黃大仙盈利大廈中層A室,實用面積307平方呎,建築面積459平方呎,屬兩房一廳間隔,向西南,單位附設典雅裝修,以$418萬易手,實用面積平均呎價$13,616,建築面積平均呎價$9,107。

-- 北角寶馬臺中層戶 減價$50萬易主 --

世紀21日昇地產執行董事黃文龍表示,新近錄得北角寶馬臺中層P室成交,單位實用面積738平方呎,建築面積864平方呎,3房連套房間隔,附設露台,座向東南望全山景,連1個車位,原業主開價$1,100萬,經議價後以$1,050萬成交,實用面積平均呎價$14,228,建築面積平均呎價$12,153,其成交價略低市價5%。

-- 天水圍嘉湖山莊三房 $1.2萬租出 --

祥益地產分行主管林家倫表示,最近錄得天水圍嘉湖山莊樂湖居1座低層A室,實用面積636平方呎,建築面積818平方呎,三房兩廳,附設企理裝修及全屋傢電,日前獲一名外區客以$1.2萬租入,實用面積平均呎租$18.9,而建築面積平均呎租$14.7。

-- 天水圍天富苑低層 自由市場價$335.5萬易手 --

祥益地產分行主管林家倫表示,日前錄得天水圍天富苑J座低層8室,實用面積506平方呎,建築面積665平方呎,兩房兩廳,獲區內新婚上車客以$335.5萬(自由市場價)購入,實用面積平均呎價$6,630,而建築面積平均呎價$5,045,屬市場價成交。

-- 東環II加推129伙於本周六發售 --

新地發展的東環 II舉行記者會,公布項目最新部署。新地副董事總經理雷霆宣布,因有見特色戶反應理想,故加推第1期東環單位,包括餘下特色單位,其推出其中19伙以及2期東環II推出 129伙,整個項目共推148伙安排本周六(19日)發售。新地代理助理總經理胡致遠指,是次發售的148伙1房折實入場約$380餘萬,另首度推出向東的3房(連套房)單位,今輪包括17伙特色戶。他又透露,東環新價單中,部分單位加價約2%至8%。

-- 維港‧星岸1、2座封盤 星海譽接力 --

長實地產旗下的紅磡維港‧星岸,昨晚公布銷售安排,停售兩張銷售安排內23伙單位。長實地產投資董事郭子威宣布,項目1座及2座已推出單位累沽逾100伙,售出約八成,戶戶成交價逾2,000萬元,宣布1、2座正式封盤。郭氏又宣布,項目將接力推出從未推售的單邊第5座單位,並命名為「星海譽 STAR No.5」,涉78伙,包括3房及4房,實用面積706至1,358平方呎。為準備下一波推售,項目位於紅磡置富都會的示範單位明天(16日)起暫停開放,預計下星期重開。

三地產焦點簡介:逢星期三刊登,為 28Hse 的會員帶來一系列地產資訊,包括講述地產近日最熱門話題、樓市成交及新盤動向等。熱門話題主要是以年輕、草根市民的角度出發,分析香港置業的困難、樓市高低對他們的影響,以冀道出大部分香港市民的心聲。